Rental yield, essentially, tells you how much you can expect to earn from an investment property that you’re renting out. It’s typically expressed as a percentage of the cost of the property. You can use this figure to determine if a property you’re thinking about buying would be a good investment or to understand your return on investment (ROI) in a property you already own. This figure is also helpful if you’re trying to decide if a “buy-to-let” mortgage is affordable for you. To work out the rental yield, you need to know the total costs of buying and owning the property as well as the amount of rent you’ll collect.X

StepsMethod 1Method 1 of 3:Totaling Property Costs

1Calculate your yearly mortgage payments. If you have a mortgage on the property, total the mortgage payments you would make over the course of a year, including interest, taxes, and any associated fees. These payments are part of your cost of owning the property.XEven if you don’t have a mortgage, you’re likely still responsible for property taxes on the property. Those would also be considered part of your costs of ownership.If you don’t own the property yet, use an estimate of mortgage payments or get an offer from a mortgage company for the property and use that number instead.

2Get a quote for insurance. If you rent out the property, you’ll typically need landlord insurance, which may have different rates than homeowner’s insurance. If you don’t already own the property, a quote from a reputable insurer will help you estimate this cost.XIn addition to landlord’s insurance, you may also want to consider other types of insurance to cover damage to the property.Rent insurance may also be available to you, which provides you some money in the event your tenant breaks their lease or needs to be evicted for nonpayment of rent.

3Include any management fees or other property expenses. If you’ve hired a management company to run the property on your behalf, their fees are considered part of your costs. You may also have other property expenses or fees, depending on where the property is located.XFor example, if you only own the building but not the land, you may have to pay rent for the land that the property sits on.If you have a unit in an apartment building or condominium complex, you may also have association fees to consider.

Tip: Include in this category expenses you might incur in the event you have to advertise for a tenant. Fees for listing the property or doing background checks on tenants are also costs of owning and renting the property.

4Estimate costs for repairs and maintenance. Over the course of the year, your tenant may have things break that need to be repaired. While you can’t necessarily predict all of these expenses, you can typically come up with a reasonable estimate based on the age of the property and its fixtures.XYou also want to consider major repairs that may be necessary in the event of a natural disaster or other event. While your insurance may cover some of this expense, you’ll likely still have to pay a deductible.Method 2Method 2 of 3:Determining Gross Rental Yield

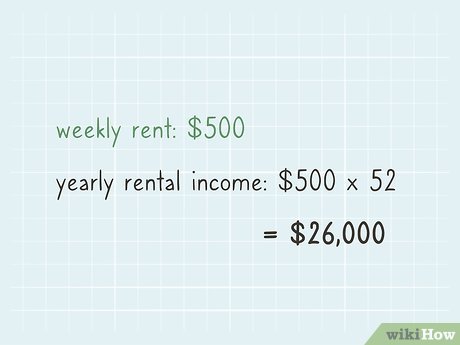

1Total your yearly rental income. Evaluate how much you charge in rent, then multiply that amount to get the total rent you’ll collect each year. If you collect weekly rent, multiply the weekly rent amount by 52. For monthly rent, multiply by 12.XFor example, if you rent the property out for $500 a week, you would have an annual rental income of $26,000.

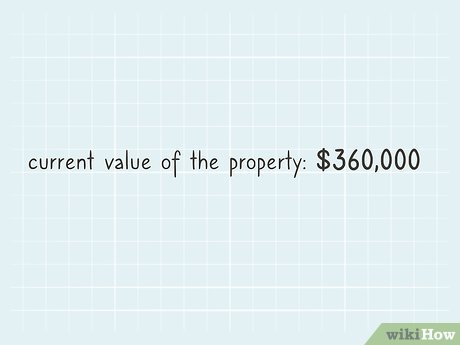

2Find the current value of the property. If you plan to purchase the property this year, the value of the property would be equal to your purchase price. However, if you already own the property, use the most recent appraisal to determine the current value.XIf you’re looking at a property for sale, use the asking price as the value of the property, even if you think the asking price is too high and plan to make a lower bid on it.

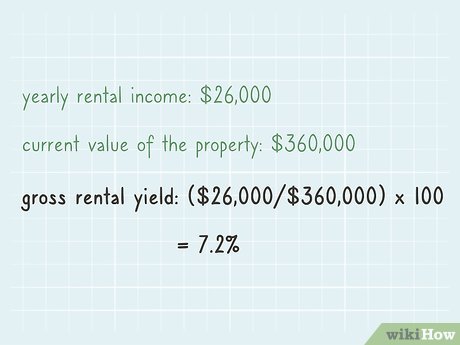

3Divide the rental income by the value to find the gross rental yield. Once you have those two figures, complete the equation. Your result will be a decimal value. Multiply that number by 100 to get a percentage.XFor example, if your yearly rental income is $26,000 and the property is valued at $360,000, you have a gross rental yield of 7.2%. Gross rental yield is considered ideal if it’s somewhere between 7 and 9%, so the gross rental yield for that property is good. Any lower than that, and you likely wouldn’t have the cash flow in the event emergency repairs were needed.

Warning: While gross rental yield is easy to calculate, it doesn’t take a lot of other factors into account that can affect the investment value of a property, such as the property’s location, age, or condition.

Method 3Method 3 of 3:Calculating Net Rental Yield

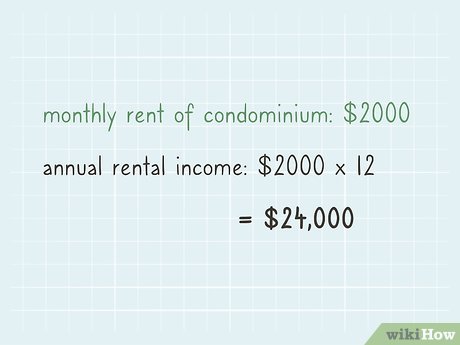

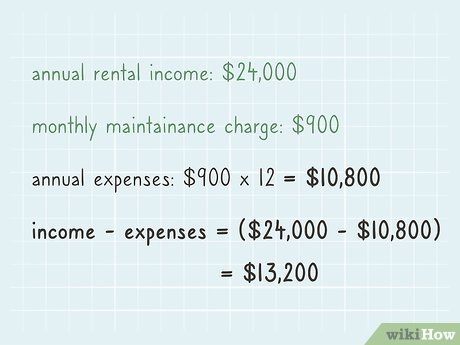

1Start with your total yearly rental income. Just as when working out gross rental yield, you’ll need the total rent you collect from the property in a year. Multiply weekly rent by 52 and monthly rent by 12 to find the annual amount.XFor example, if you rented a condominium for $2,000 a month, your annual rental income would be $24,000.

Tip: Net rental yield is typically calculated at the end of the year, looking back at real numbers. If the property was vacant for any period during the year, don’t include the rent you would have received for that time in your yearly rental income total.

2Subtract your annual expenses from the rental income. For net rental yield, you’ll also take into account the other costs of owning the property. Include all fees, mortgage payments, interest, taxes, insurance premiums, and other costs associated with the property for the year. Typically these will be monthly expenses, so don’t forget to multiply them by 12 to get the annual total.XFor example, suppose your annual rental income was $24,000 and the condominium unit cost you $900 a month to maintain. Your annual cost to own the property would be $10,800. When you subtract $10,800 from $24,000, you get $13,200.

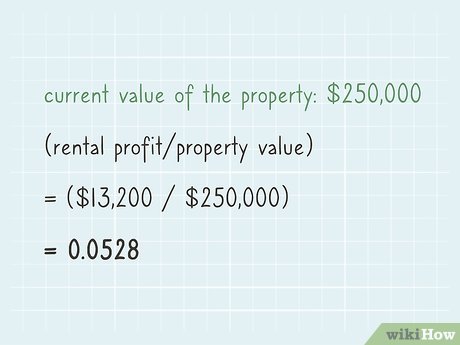

3Divide the result by the current value of the property. The current value of the property is not your mortgage payment, which likely includes interest, taxes, and other fees. Instead, look at the value of the most recent appraisal of the property. That’s the amount you could likely sell the property for.XFor example, suppose the condominium you own is worth $250,000. You have an annual rental income of $24,000 for the property, which decreased to $13,200 by the costs of owning the property. When you divide $13,200 by $250,000, you get 0.0528.

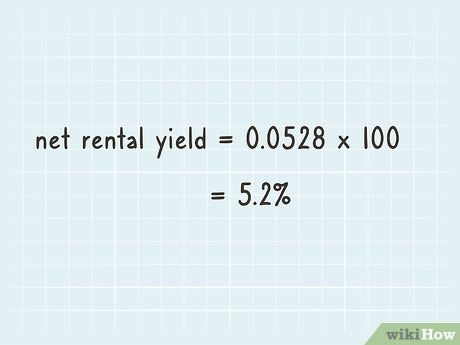

4Multiply by 100 to find your net rental yield. Net rental yield, like gross rental yield, is expressed as a percentage of the value of the property. To get that percentage, take the decimal you got when you divided the annual rental income less costs by the current value of the property and multiply it by 100.XTo continue the example, if you had annual rental income less costs of $13,200 divided by $250,000, you would have a net rental yield of 5.28%. This is considered a relatively low rental yield, but might still be sustainable depending on the location of the property or your reasons for owning it.