The statement of cash flow is part of a business’s financial report, typically completed once a year. The information on the statement of cash flow can be compiled using one of 2 accounting methods, direct or indirect. With the indirect method, you start with the business’s net income from the income statement, then adjust that amount depending on the business’s operating, financing, and investing activities. The indirect method is simpler than the direct method for businesses that keep records on an accrual basis, accounting for revenue when earned and expenses when incurred.X

StepsPart 1Part 1 of 4:Determining Operating Net Cash Flow

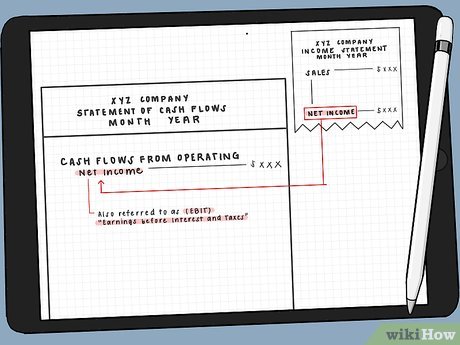

1Start with the net income listed on the income statement. The income statement you prepared as part of your company’s financial report includes a net income line. List the amount first in the operating section on your statement of cash flow.XNet income is also referred to as “earnings before interest and taxes,” abbreviated EBIT.

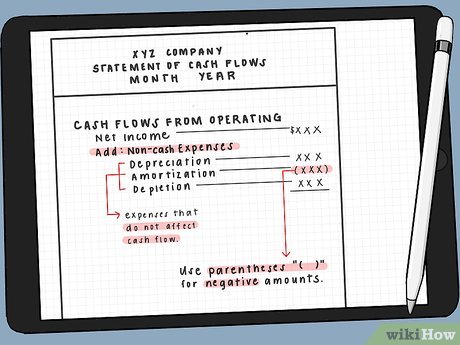

2Add expenses that don’t affect cash flow back into income. Expenses such as depreciation, amortization, and depletion reduce your company’s profit even though they don’t affect cash flow. Since you’re preparing a statement of cash flow, these expenses are added back into the net income.XIf one of the expenses is a negative amount, put the amount in parentheses on your statement.When you add the expenses back into the net income, either subtract the amounts in parentheses or add negative numbers to arrive at the correct income total.

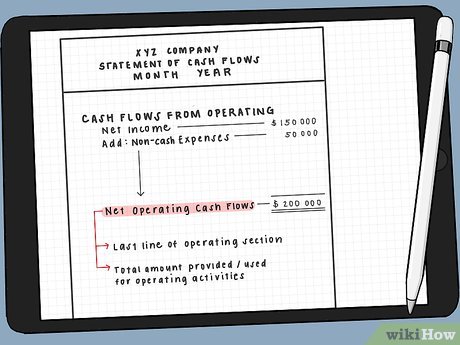

3List the total as net operating cash flow. Find your company’s net operating cash flow by adding together the net income and the non-cash expenses. This amount, listed on the last line of the operating section of your statement of cash flow, is the total amount of cash provided by or used in your company’s operating activities.XFor example, if your company’s net income is $150,000 and your total non-cash expenses are $50,000, you would have a net operating cash flow of $200,000.Part 2Part 2 of 4:Presenting Net Cash Flows from Investing Activities

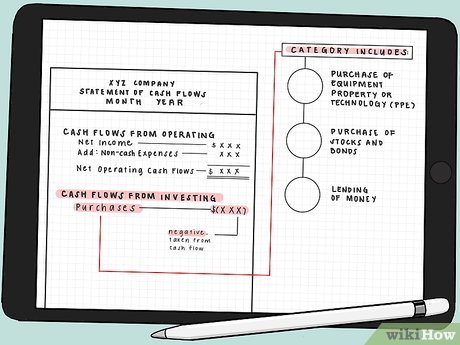

1Total any money spent purchasing capital assets or investment instruments. If your company purchased any fixed assets, including real estate, equipment, or technology, the total amount is listed on this line. Since this amount is money taken from cash flow, it’s a negative number, enclosed in parentheses. This category typically includes:XPurchases of equipment, property, or technology (typically abbreviated “PP&E,” which stands for “property, plant, and equipment”)Purchases of stocks and bondsLending of money

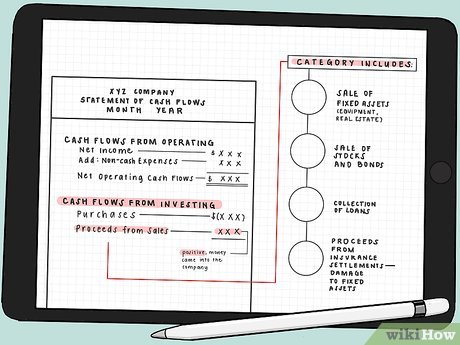

2List proceeds from sales of any capital assets or investments. This line represents positive cash flow, money that came into your company as a result of investing activities. The following types of activities are typically included here:XSales of fixed assets, including equipment or real estateSales of stocks and bondsCollection of loansProceeds from insurance settlements related to damage of fixed assets

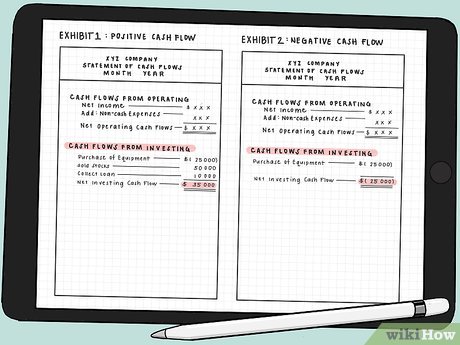

3Compute the net cash used in investing activities. Add the positive and negative investing cash flow items together to find the net investing cash flow. This number might be expressed as either a positive or negative amount.XFor example, if your company purchased equipment totaling $25,000, sold stocks for $50,000, and collected a $10,000 loan, it would have $35,000 in net investing cash flow (-$25,000 + $50,000 + $10,000 = $35,000).On the other hand, if your company purchased equipment totaling $25,000 but didn’t have any positive cash flow related to investing activities, your company would have a net investing cash flow of -$25,000 or ($25,000).Part 3Part 3 of 4:Including Net Cash Flows from Financing Activities

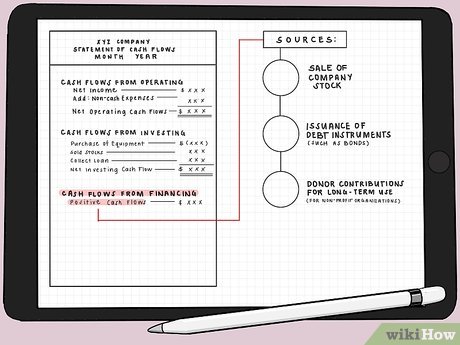

1List transactions in which funds were provided to the company. For larger companies, these transactions, expressed as positive cash flow, can be a substantial source of money coming into the company. Items listed as positive cash flow from financing activities include:XSales of company stockIssuance of debt instruments, such as bondsDonor contributions for long-term use (for a nonprofit organization)

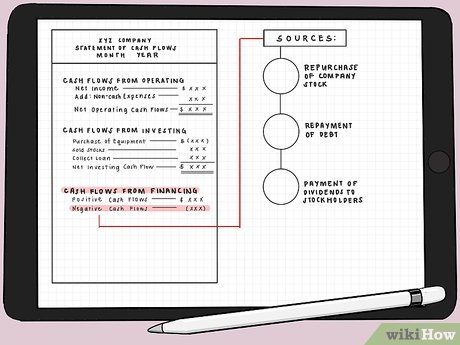

2Provide the amount of money that was returned to owners or lenders. These transactions involve money that the company paid to owners or lenders, with the amount expressed on the statement in parentheses. Small businesses that don’t issue dividends and have little debt may not have any negative financing cash flow. The following items might be included in this total:XRepurchase of company stockRepayment of debtPayment of dividends to stockholders

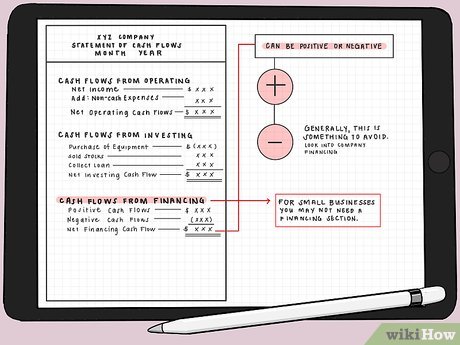

3Add all entries together to get your net financing cash flow. Combine the lines in this section just as you did in the operating and investing sections. The resulting net financing cash flow could be positive or negative. Generally, you want to avoid having a negative net financing cash flow, particularly if it isn’t significantly offset by positive operating and investing cash flows.XIf this amount is negative, you may need to look into your company’s financing in more detail — particularly if your company is trying to manage a significant amount of debt.If you have a relatively small business that doesn’t issue dividends or have any debt, you may not need a financing section in your statement of cash flows at all.Part 4Part 4 of 4:Reconciling Beginning and Ending Cash Balances

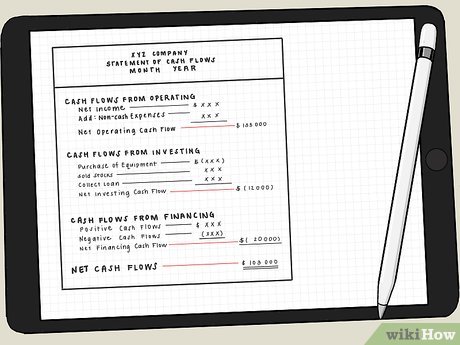

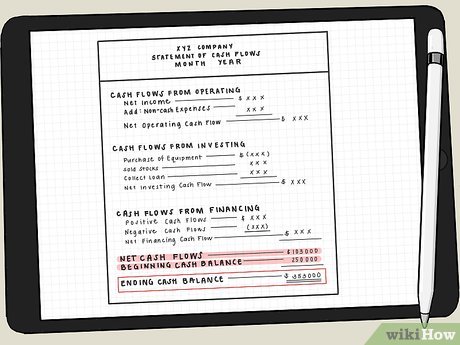

1Combine net cash flows from operating, financing, and investing activities. Take the last 3 lines of each section in your statement of cash flow and add them together. If you have negative cash flow in any category, subtract that amount (you can also add a negative number and get the same result.XFor example, if your business has $135,000 in net operating cash flow, -$20,000 in net financing cash flow, and -$12,000 in net investing cash flow, you have a positive net cash flow of $103,000 for the period (135,000 + -20,000 + -12,000 = 103,000).

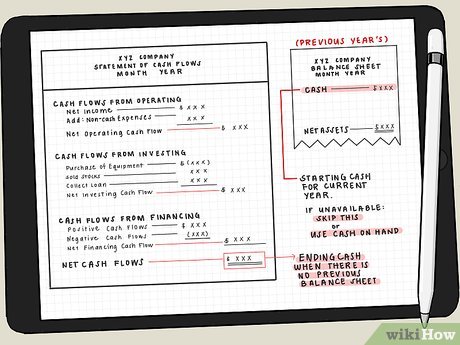

2Copy the beginning cash balance from the previous year’s balance sheet. Go to the financial statement prepared for the previous accounting period. The cash balance represents your starting cash for the period covered by this statement.XIf you don’t have a report for a previous accounting period, either use the amount of cash on hand that you started with or simply skip this step. Your ending cash balance will be the total net cash flows you calculated on your statement of cash flow for the period.

3Add the total net cash flow to the beginning cash balance. The total net cash flow you found on your cash flow statement plus the cash balance you started with is your business’s ending cash balance. List this amount on the last line of your statement of cash flow.XFor example, if your company had a beginning cash balance of $250,000 and a total net cash flow of $103,000, your ending cash balance would be $353,000 (250,000 + 103,000 = 353,000).