Accrued interest on a bond refers to the the interest that has been earned but not yet paid since the most recent interest payment. At the end of this accrual period (typically six months or a year) bonds generally pay interest. These are known as “coupon” payments. Depending on the bond, interest can be calculated in different ways. They all use what’s called a “day-count fraction” or DCF. This refers to the number of days in a month or year, a number that is standardized for any given bond. For example, many bonds calculate interest by allocating 30 days to a month and 360 days to a year. Others may use the actual number of days in a month and year. To calculate your accrued interest, you must first know which of these methods is used for your bond and then do a few simple calculations.

StepsPart 1Part 1 of 3:Gathering Your Information

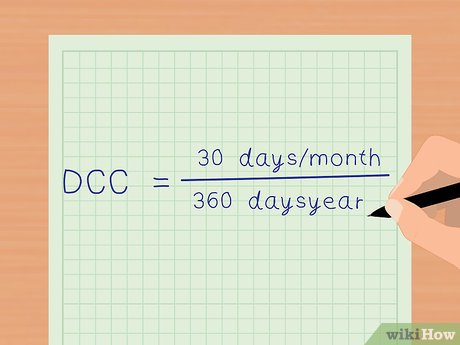

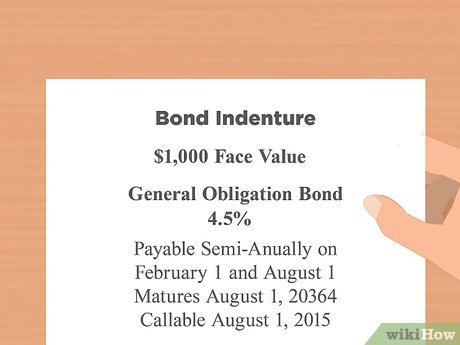

1Determine the day-count convention on your bond. The day-count convention (DCC) determines how the day-count fraction (DCF) is found when calculating accrued interest. The day-count convention on your bond is defined in the accompanying indenture (contract). X For example, 30 days in a month and 360 days in a year would mean a DCC of 30/360. Other bonds, especially U.S. government (Treasury) bonds, calculate interest using the exact number of days in a month and year. Such a DCC is sometimes referred to as “actual/actual” or “ACT/ACT.” In practice, bonds can also use a combination of these two DCCs, with such possible DCCs as 30/ACT and ACT/360. In practical terms, the convention used will make very little difference in terms of interest earned. Double-check your bond indenture to be sure. X

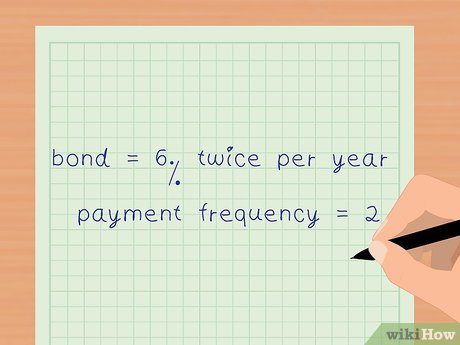

2Confirm the interest rate and payment frequency on your bond. Your interest rate, also called the the coupon rate, specifies the amount of interest you earn on the bond annually as a percentage of your par (or “face”) value. The payment frequency signifies whether your bond pays interest once a year or more often. Bonds typically pay interest either annually or semi-annually (once or twice per year). X This information can be found within your bond indenture.For example, your bond might pay a 6% coupon rate twice per year. In this case, the annual interest rate would be 6% divided by the number of payments within the year. Thus, a 6% bond that pays interest twice per year would effectively pay 3% of the par value for each of the two payments during the year, or 6% total.

3Find when the most recent coupon payment was made. Search your records to see when your bond made its latest coupon payment. This information is available from the financial institution that sold you the bond.

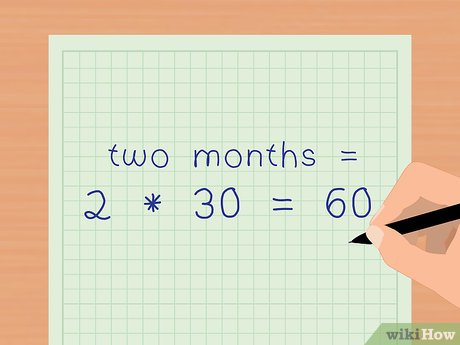

4Calculate how many days have passed since the most recent coupon-paying day. This will depend on your DCC, as the passage of days is calculated differently in each type of bond. Generally, if your bond is actual/actual, you will actually count the days. If your bond is 30/360, you would use those numbers for each month or year that has passed. XLet’s say you have a 30/360 bond, and exactly two months have passed since your latest payment. You would simply multiply 2 x 30 and use 60 days in your calculations, regardless of how many days there actually were in the elapsed months.

5Confirm the face or par value of your bond. This is the amount paid to the holder of the bond at maturity (when the interest payments stop). X This will be stated clearly on your bond indenture.Note that the par value may be more or less than what you actually paid for the bond originally. Market price is affected by the existing rate environment and the bond issuer’s creditworthiness. XBonds are often valued at $1000. That would be the par value even if you paid slightly more or less for it.Part 2Part 2 of 3:Calculating Bond Accrued Interest Manually

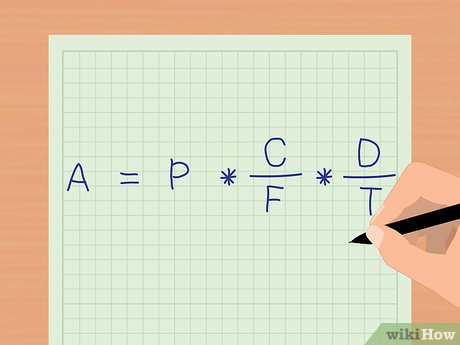

1Know the equation for bond accrued interest. It’s simpler than it looks: A=P∗CF∗DT}*}}

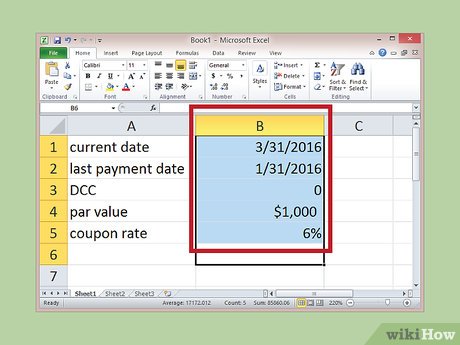

1Open Excel and create a new sheet. Start Excel on your computer and start with a blank sheet so that there is no other information to distract you.

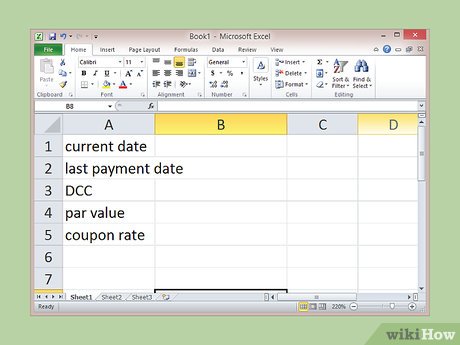

2Enter the names of the variables in the first column. For this calculation we would enter the current date, most recent payment date, DCC, par value, and coupon rate. Put these variables on separate lines down the first column of the spreadsheet. “Current date” goes in A1. “Coupon rate” lands in A5.

3Input the variables. Next to each variable name input the actual values. Make sure that these values are entered correctly. In other words, the dates are entered as dates, percentages as percentages, and monetary values as such. Otherwise, the program will not calculate the result properly. In our example, we use the following variables:3/31/2016 as the current date in cell B1.1/31/2016 as the last payment date in cell B2.0 as the DCC in cell B3. This indicates that we are using the 30/360 DCC. Inputting 1 indicates the actual/actual DCC.X$1000 as the par value in cell B4.6% as the coupon rate in cell B5.

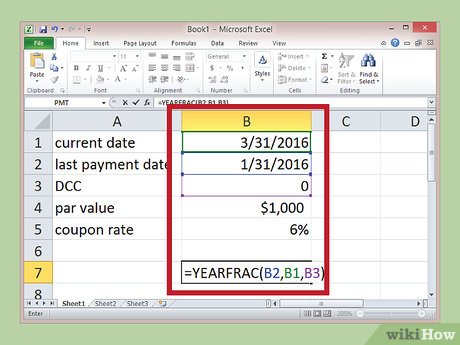

4Create the YEARFRAC function, and input the values. The function needed to calculate bond accrued interest is known as the YEARFRAC function. Click on a nearby empty cell and type “=YEARFRAC(” to get started. The system will prompt you to input variables.Click on cell B2.Type in a comma to move to the next variable.Click on cell B1.Type in a comma to move to the next variable.Click on cell B3.Close the function with a parenthesis.

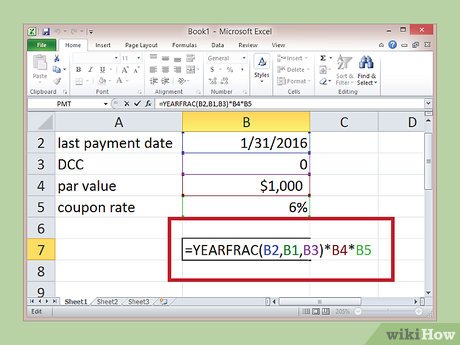

5Multiply the function by the par value and coupon rate. In the same cell as the function, after you’ve closed the function, you must multiply it by your other two variables. Simply type in “*B4*B5” directly after the function, with no spaces anywhere.Your completed entry into this cell should look like this: =YEARFRAC(B2,B1,B3)*B4*B5

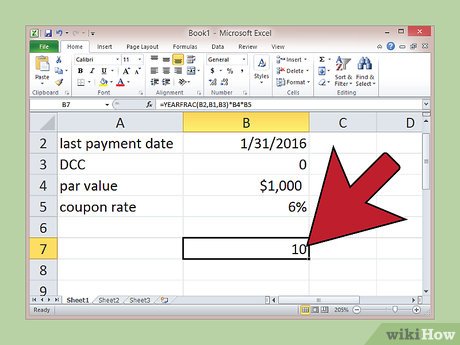

6Press enter and get your answer. The program will solve your equation when you press enter on the cell that contains your function. Be sure to adjust the type of number in the cell to “currency” by selecting it at the top of the page under “number.” This will ensure that your answer is displayed correctly.In the example, this function yields $10, which is exactly the same as it was in our manual calculation.