Probate is the legal process of collecting and distributing a person’s assets after his or her death. As attorney fees, court costs, probate fees, or taxes can be expensive, many choose to plan their estate in order to avoid probate. Avoiding probate generally means ensuring that certain assets do not become a part of your probate estate. To prevent assets from becoming a part of your estate and avoid probate in Canada, follow the steps below.

Steps

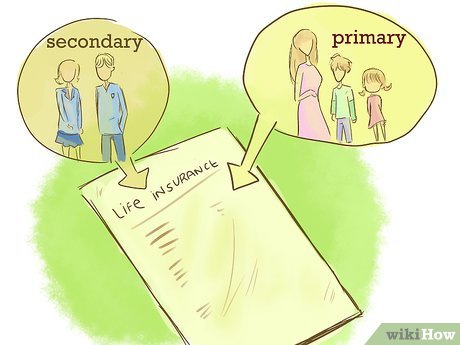

1Name beneficiaries on your life insurance policies. Life insurance is paid directly to the named beneficiary, so the funds never become a part of the probate estate, therefore not subject to probate taxes and fees.X You may also wish to name a secondary beneficiary, in case the primary beneficiary predeceases you.

2Hold your assets in cash and/or bearer certificates. Assets held in cash or bearer certificates, such as stock, may be excluded from the probate estate, reducing the amount of fees and taxes charged to it. A bearer certificate is a financial instrument, such as a check payable to ‘cash’, which may be redeemed by any party possessing it.

3Add a Pay on Death (“POD”) or Transfer on Death (“TOD”) designation to your accounts. This can only be done in the USA. Canada does not have such a law for non-registered investment accounts. Only registered accounts such as an RRSP, RRIF, TFSA accounts can have named beneficiaries. Joint ownership is the only way to avoid probate for non-registered accounts.XA POD or TOD designation allows you to decide to whom the property will transfer or be paid upon your death. As it will be paid or transferred directly to the designated party, it will not be subject to probate taxes.X To name a POD or TOD, contact the bank or investment firm where the account is held. The procedure will vary from company to company and will most often involve filling out and returning a simple form.

4Title your assets to a joint owner. Assets, which are held jointly with rights of survivorship, pass directly to the surviving joint owner, and never become subject to probate.X Joint ownership is not right in all circumstances. You may wish to consider the following, before naming a joint owner of any of your assets.A joint owner can clean out your accounts or otherwise encumber your property. Once a party owns an interest in your property, he or she may take out loans against it, or in the case of a bank or investment account, empty it. This can be done without your knowledge or consent.You will need the cooperation of the joint owner in order to sell or mortgage the property. Once you name a joint owner, he or she will need to consent to any sale of the property, or any mortgage taken against it.Naming a joint owner, when he or she is not the only beneficiary of the estate, may cause discontentment between heirs. The other beneficiaries may believe that the joint owner was only meant to hold the property in trust for all of the beneficiaries, and a dispute as to who should inherit the property can easily arise.There may be tax consequences, such as capital gains property transfer tax, when naming joint owners of certain property. You may want to consult with a Certified General Account (“CGA”) or tax attorney before doing anything that may affect your obligation to pay taxes.Just as a joint owner has a claim to the joint property, so does his or her creditors. Titling your property with another as a joint owner may subject it to the claims of the joint owner’s creditors and/or his or her spouse.

5Give gifts.X Gifting your property now will reduce the value of the estate at your death, thereby reducing the amount of taxes and/or fees due. Be aware that certain legal requirements and/or obligations may apply when making inter-vivos gifts or to those made while you are alive, for the purpose of reducing probate taxes. These considerations include:You must actually give up control of the gift to the giftee. For example, if you make a gift of an antique piece of furniture, you must deliver the piece to the giftee, and discontinue your possession of it. Another example is if you bestow a bank account upon another, you must add their name and remove yours from the title.There may be tax consequences for the one who receives the gift. For example, if the fair market value (“FMV”) of the gift exceeds its cost, the accrued gain may be taxable as a capital gain. The Canadian Revenue Agency (“CRA”) defines FMV as “the highest price, expressed in dollars, that a property would bring in an open and unrestricted market, between a willing buyer and a willing seller who are both knowledgeable, informed, and prudent, and who are acting independently of each other.”XProperty tax transfer and other fees may be due when gifting real estate to another. You may wish to consult with a CGA, tax attorney, or probate lawyer before transferring any real property to another party, in order to ensure that your legal and financial rights are protected.X

6Set up a trust. A trust allows you to title your property to it, to be held by an appointed trustee, on your behalf. You may appoint yourself as trustee if you choose. The trust will provide for the distribution of the property after your death. Since the property is owned by the trust, it never becomes a part of your probate estate and is not subject to probate taxes.X

7Title assets to your company. If you have outstanding debt other than a mortgage, that debt will not be subtracted from your assets when the value of your estate at the time of your death is determined. This will increase the value of your estate, causing a higher probate tax to apply. Transferring the loan and the asset purchased with it to a limited company will reduce the gross value of your estate, which in turn will reduce the amount of probate tax due.

8Make two wills. Parties who hold certain assets may decide to make two wills. A Primary Will, which deals with those assets that are required to be subject to probate, and a Secondary Will, which provides direction as to the distribution of all other assets. While this is not a widely known practice, the Court in Ontario recently approved of this estate planning approach in Granovsky Estate v. Ontario.X