A forward contract is a type of derivative financial instrument that occurs between two parties. The first party agrees to buy an asset from the second at a specified future date for a price specified immediately. These types of contracts, unlike futures contracts, are not traded over any exchanges; they take place over-the-counter between two private parties. The mechanics of a forward contract are fairly simple, which is why these types of derivatives are popular as a hedge against risk and as speculative opportunities. Knowing how to account for forward contracts requires a basic understanding of the underlying mechanics and a few simple journal entries.

StepsPart 1Part 1 of 3:Accounting for Forward Contracts

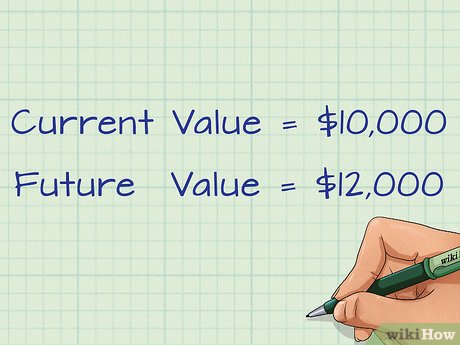

1Recognize a forward contract. This is a contract between a seller and a buyer. The seller agrees to sell a commodity in the future at a price upon which they agree today. The seller agrees to deliver this asset in the future, and the buyer agrees to purchase the asset in the future. No physical exchange takes place until the specified future date. This contract must be accounted for now, when it is signed, and again on the date when the physical exchange takes place.XFor example, suppose a seller agrees to sell grain to a buyer in 3 months for $12,000, but the current value of the grain is only $10,000. In one year, when the exchange takes place, the market value of the grain is $11,000, so in the end, the seller makes a profit of $1,000 on the sale.The spot rate, or current value, of the grain is $10,000.The forward rate, or future value, of the grain is $12,000.

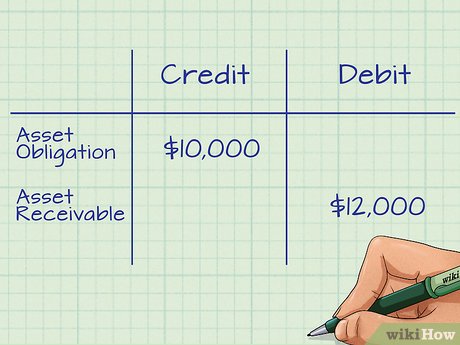

2Record a forward contract on the contract date on the balance sheet from the seller’s perspective. On the liability side of the equation, you would credit the Asset Obligation for the spot rate. Then, on the asset side of the equation, you would debit the Asset Receivable for the forward rate. Finally, debit or credit the Contra-Asset Account for the difference between the spot rate and the forward rate. You would debit, or decrease the Contra Asset Account for a discount and credit, or increase it for a premium.XUsing the example above, the seller would credit the Asset Obligation account for $10,000. He has made a commitment to sell his grain today, and today it is worth $10,000.But, he is going to receive $12,000 for the grain. So he debits Assets Receivable for $12,000. This is what he’s going to be paid.To account for the $2,000 premium, he credits the Contra-Asset Account for $2,000.

3Record a forward contract on the contract date on the balance sheet from the buyer’s perspective. On the liability side of the equation, you would credit Contracts Payable in the amount of the forward rate. Then you would record the difference between the spot rate and the forward rate as a debit or credit to the Contra-Assets Account. On the asset side of the equation, you would debit Assets Receivable for the spot rate.XUsing the example above, the buyer would credit Contracts Payable in the amount of $12,000. Then he would debit the Contra-Assets Account for $2,000 to account for the difference between the spot rate and the forward rate.Then he would debit Assets Receivable for $10,000.

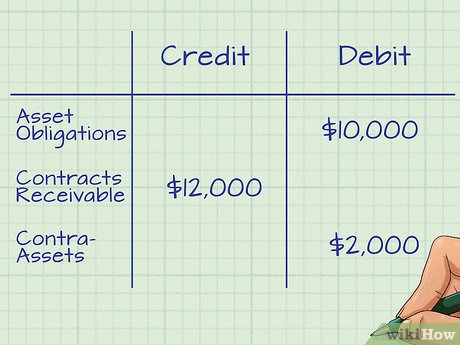

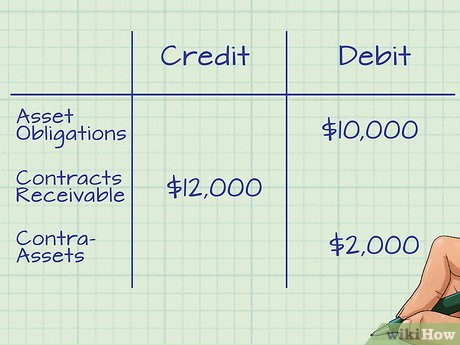

4Record a forward contract on the balance sheet from the seller’s perspective on the date the commodity is exchanged. First, you close out your asset and liability accounts. On the liability side, debit Asset Obligations by the spot value on the contract date. On the asset side, credit Contracts Receivable by the forward rate, and debit or credit the Contra-Assets account by the difference between the spot rate and the forward rate.XUsing the above example, on the liability side you would debit Asset Obligations by $10,000.On the asset side, you would credit Contracts Receivable by $12,000/Then you would debit the Contra-Asset account by $2,000, the difference between the spot rate and the forward rate.

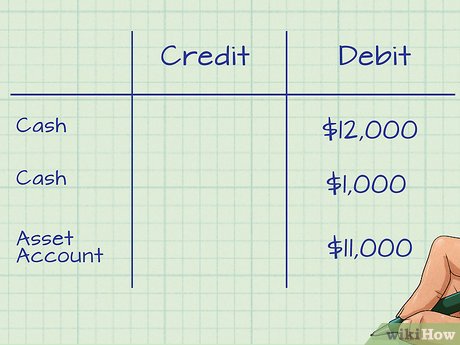

5Recognize any gain or loss on the commodity sold from the seller’s perspective. Determine the current market value of the commodity. This is its value on the date of the physical exchange between the buyer and seller. Next, debit, or increase, your cash account by the forward rate. Then credit, or decrease, your Asset account by the current market value of the commodity. Finally, recognize the gain or loss, which is the difference between the forward rate and the current market value, with a debit or credit on the Asset Account.XIn the example above the current market value of the grain on the date of the physical exchange is $11,000.First, the seller must increase cash based on the contracted amount, so he would debit cash by $12,000.Next he must reduce the Asset account by the current market value by recording a credit of $11,000.Then, to recognize the gain of $1,000 (which is the current value, $11,000, less the spot rate, $10,000), he would record a credit on the Asset Account of $1,000.

6Record a forward contract on the balance sheet from the buyer’s perspective on the date the commodity is exchanged. First, you close out your asset and liability accounts. On the liability side, debit Contracts Payable by the forward rate, and debit or credit the Contra-Assets account by the difference between the spot rate and the forward rate. On the asset side, credit Assets Receivable by the spot rate on the date of the contract.XUsing the example above, on the liability side, the buyer would debit Contracts Payable by $12,000 and credit the Contra-Asset Account by $2,000.On the asset side, he would credit Assets Receivable by $10,000.

7Recognize any gain or loss on the commodity sold from the buyer’s perspective. Decrease, or credit the Cash account by the amount of the forward rate. Then, record the difference between the forward rate and the current market value as an additional credit or debit to the Cash account. Finally, increase, or debit, the Asset account by the current market value of the commodity.XIn the above example, the buyer would debit Cash by $12,000.The difference between the market value, $11,000, and the forward rate $12,000, is $1,000. They buyer lost $1,000, so he would record a debit to Cash of $1,000.Next, he would debit the Asset account by $11,000.Part 2Part 2 of 3:Understanding Forward Contracts

1Understand the definition of a forward contract. A forward contract is an agreement between a buyer and a seller to deliver a commodity on a future date for a specified price. The value of the commodity on that future date is calculated using rational assumptions about rates of exchange. Farmers use forward contracts to eliminate risk for falling grain prices.X Forward contracts are also used in transactions using foreign exchange in an effort to reduce the risk of losses due to changes in the exchange rates.

2Learn the meaning of derivatives. A derivative is a security with a price that is based upon, or derived, from something else. Forward contracts are considered derivative financial instruments because the future value of the commodity is derived from other information about the commodity.XThe future value of the commodity for the forward contract is derived from the current market value, or spot price, and the risk-free rate of return.

3Learn the meaning of hedging. In investing, hedging means minimizing risk. In forward contracts, buyers and sellers attempt to minimize risk of losses by locking in prices for commodities in advance. Buyers lock in a price in hopes that they will end up paying less than the current market value of a commodity. Sellers hedge their risks with forward contracts in an attempt to protect themselves from falling prices.XPart 3Part 3 of 3:Negotiating a Forward Contract

1Know the difference between the long position and the short position. The party agreeing to purchase the commodity assumes the long position. The party agreeing to sell the commodity is assuming the short position.XThe buyer, who is in the long position, is the person who stands to benefit if the price of the commodity rises higher than expected.The seller, who is in the short position, stands to lose if the price of the commodity rises.

2Know the difference between the spot value and the forward value. The spot value and the forward value are both quotes for the rate at which the commodity will be bought or sold. The difference between the two has to do with the timing of the settlement and delivery of the commodity. Both parties in a forward contract need to know both values in order to accurately account for the forward contract.XThe spot rate is the current market value for the asset in question. It is the value of the commodity if it were sold today. For example, a farmer selling grain for the spot value agrees to sell it immediately for the current price.XThe forward rate is the agreed-upon future price in the contract. For example, suppose the farmer in the above example wants to enter into a forward contract in an effort to hedge against falling grain prices. He can agree to sell his grain to another party in six months at agreed-upon forward rate. When the time comes to sell, the grain will be sold for the agreed-upon forward rate, despite fluctuations that occur in the spot rate during the intervening six months.X

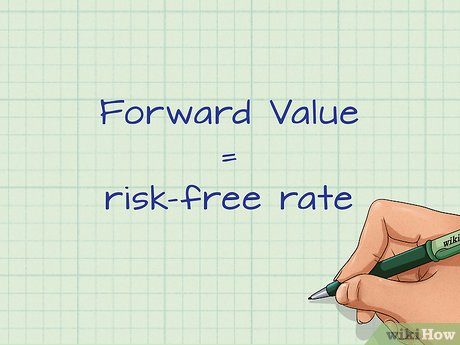

3Understand the relationship between the spot value and the forward value. The spot rate can be used to determine the forward rate. This is because a commodity’s future value is based in part on its current value. The other factor that is used to determine the forward value is the risk-free rate.XThe risk-free rate is the rate at which the commodity is expected to change in value with zero risk. It is usually based on the current interest rate of a three-month U.S. Treasury bill, which is considered the safest investment you can make.X