Saving money can be a challenge when you’re raising a family on a single income, but you can still find ways to stretch your funds to fit your budget. Start by cutting out any purchases you don’t need to make and saving money you didn’t spend. Then compare your income to what you spend each month so you can plan a budget. If you still want to put aside more money, you may need to find ways to increase your income. With a bit of planning and changes in your lifestyle, you can start saving money for yourself and your family!

StepsMethod 1Method 1 of 3:Cutting Costs Immediately

1Get rid of unnecessary purchases or subscriptions you have. Limit the number of impulse purchases you make since you’re spending money that you can save instead. Look for subscriptions you have, such as streaming services like Netflix or Hulu, and ask yourself how often you actually use them. If you only use it once or twice a month, then cancel the service. Only spend your money on items you need and bills you have to pay so you have extra income to set aside.XExpert Source![]() Samantha Gorelick, CFP®Financial PlannerExpert Interview. 6 May 2020.For example, avoid buying coffee or drinks while you’re out. Instead, bring your own drinks since it’s much cheaper.It’s okay to make a few small impulse purchases every so often, but don’t let it become a habit.

Samantha Gorelick, CFP®Financial PlannerExpert Interview. 6 May 2020.For example, avoid buying coffee or drinks while you’re out. Instead, bring your own drinks since it’s much cheaper.It’s okay to make a few small impulse purchases every so often, but don’t let it become a habit.

2Make a list before you go shopping so you don’t overspend. While you’re at home, write down a list on a piece of paper or on your phone. Look around your home to see what you need so you can add it to your list before you leave. Once you’re at the store, only get the items you wrote on your list so you don’t impulsively buy anything. Cross things off your list once you buy them so you don’t accidentally buy them again.X

3Plan meals in advance so you know what you need from the grocery store. Cooking a meal at home is much cheaper than taking your family out for dinner. Look online or through cookbooks and pick out a few healthy recipes that you want to make for the week. Write down all the ingredients that you need and go grocery shopping for the things you don’t already have. Plan meals for a week in advance so you always know what items you need to buy.XFor example, you can make meals like chili, vegetable stir fry, pot roast, or grilled chicken.X

4Check for coupons or discount codes to save money at stores. Look through newspapers, store circulars, and online for coupons that you can use on your purchases. If the coupons are for items that you need, cut them or write down the discount code so you can save money on your purchase. Check for any additional sales that the store may be having and make note of any items you need that are discounted.XDon’t buy items that you don’t need just because you have a coupon for it.Some coupons and discount codes may only work online or at certain locations.Check for online services that sign you up for coupons and store rewards since they can help you save more money while you’re shopping.

5Look at thrift stores for cheaper used items. Rather than shopping for name-brand products, look for cheaper generic brands to save money. Go to secondhand stores or thrift shops to look for cheap clothes, accessories, and other products. On top of selling used items, some thrift stores also sell new items that are much cheaper than other stores. Make sure you only buy the things you need so you don’t overspend.X

Tip: You can also donate products to the thrift store that you don’t use anymore since you may be able to get tax deductions.

6Create fun traditions for holidays and birthdays rather than buying gifts. If you don’t have a lot of extra money to buy a lot of gifts, make holidays and birthdays special by celebrating in different ways. It may be difficult to stop giving gifts, but you can go somewhere special, make homemade cakes and desserts together, or spend a night at home doing your children’s favorite things. Make memories together so you can still have a fun time even if there aren’t gifts involved.Try saving a little bit of money throughout the year so you have some to spend on gifts around birthdays and holidays.

7Say no when your children ask for something you can’t afford. If your child asks you to buy something for them, tell them no and explain that you don’t have enough money to. It may be hard for them to understand, but talk to them about how it’s important to save money and that you need to use the money for food and other things. Tell them if they want to get it, that they need to save their own money for it.XKeep in mind what your child says they want since you may be able to save money and get it for them as a gift.Method 2Method 2 of 3:Setting Your Budget![]()

1Create a monthly budget so you can see where you’re spending your money. Write your budget on a piece of paper or start a spreadsheet online so it’s organized and easy to access. Write down the total amount of income you receive monthly in one column and list all your expenses in another column. Start with fixed expenses, like bills, rent, and child care, then list your variable expenses, such as groceries, gas, haircuts, and entertainment. Set certain amounts for your variable expenses so you can still put some of your money aside.XExpert Source![]() Samantha Gorelick, CFP®Financial PlannerExpert Interview. 6 May 2020.Check your bank statement from the previous month to look at everything you spent money on to help you see what purchases you can cut.Make a weekly budget if you want to get more detailed and in-depth with how you spend your money.

Samantha Gorelick, CFP®Financial PlannerExpert Interview. 6 May 2020.Check your bank statement from the previous month to look at everything you spent money on to help you see what purchases you can cut.Make a weekly budget if you want to get more detailed and in-depth with how you spend your money.

2Pay off your bills in full to maintain a good credit record. Look for regularly occurring bills in your budget and make sure they are fully paid. This may include utilities, rent, student loans, credit card payments, or mortgages. Take money out of your income equal to the amount you need for your bills since your credit record will start to go down if you miss payments.XExpert Source![]() Samantha Gorelick, CFP®Financial PlannerExpert Interview. 6 May 2020.Keep a calendar with all the days your bill payments are due so you don’t forget or miss any dates.

Samantha Gorelick, CFP®Financial PlannerExpert Interview. 6 May 2020.Keep a calendar with all the days your bill payments are due so you don’t forget or miss any dates.

Tip: Ask utility companies if they can offer lower rates or discounts. They may be able to find you deals so they don’t lose a customer.X

3Prioritize money for an emergency fund. You can never predict if you run into car trouble or lose a job, so start putting money into an emergency savings account. Aim to save at $50-100 USD a month if your budget allows you so you can build your fund quickly. Keep saving money until you have at least 3 times your monthly expenses so you can afford to live if something happens.XDon’t pull money out of the emergency fund if you don’t have to. Try to leave it alone as much as you can so your money adds up.

4Set some of your income aside for a retirement fund. While it’s important to provide for your family, it’s also important to put money aside for your future. Do your best to set aside at least 10% of your income into a retirement fund so you’re able to live comfortably when you’re older.X Make sure you can afford any of your other set expenses and bills before putting money into your retirement fund.XCheck if your employer offers retirement benefits since they may be able to set aside some of your income into a fund before it even goes on your paycheck. Some employers may also match certain retirement contributions to help your funds grow faster.

5Look into a college savings plan for your children. Apply for and start a 529 college savings plan in your state so you can start setting money aside for your children. Put a bit of money aside from your income into the savings account so it can build interest and grow over time. The money inside a college savings fund has tax-free growth and withdrawals as long as you use it for your children’s educational expenses.XAsk family members and friends to add to the savings plan as a gift for you or your children so they can use the money for college.See if you can divert some of your income directly into the savings account before you receive your paycheck so it’s easier to put money away.

6Avoid relying on credit cards for financial support. Using credit cards repeatedly can lower your credit record if you’re unable to make your payments or if you have a large outstanding balance. Keep a credit card only if you’re able to make regular payments on it and it’s for emergencies. If you already have credit cards, try to pay them off as fast as you can and set them aside so you don’t use them regularly and so you maintain your credit record.XMethod 3Method 3 of 3:Earning Additional Income![]()

1Ask your employer for a raise. If you still don’t make enough income to live comfortably, ask if your employer will meet with you privately. While it can be difficult to ask for a raise, give specific reasons why you think you deserve the additional money based on your work ethic or time you’ve spent on the job. Be confident while you talk with your employer and answer any questions they have for you. No matter what they say, thank them for their time and consideration.XAsk for a raise when your manager is in a good mood or after you’ve completed an important project since you might be more likely to get it.

Tip: Even if your employer can’t give you a raise, see if they can offer other benefits, such as insurance or childcare.

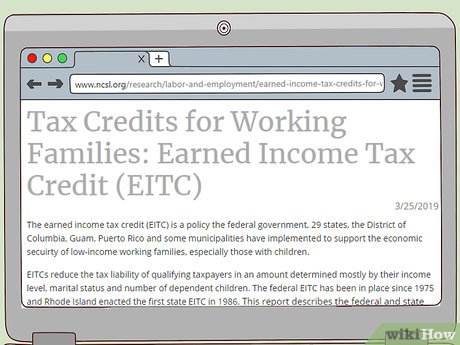

2Claim earned income tax credit to pay less on your taxes. Single parents can get special deductions on their federal and state taxes and get more in their tax return. Check online for your eligibility for earned income tax credits (EITC) since you may be able to get more on your tax return when you file. Complete the EITC paperwork forms, which is usually 1040A or Form 1040, and include them in your tax return.XTrustworthy SourceNational Conference of State LegislaturesBipartisan, nongovernment organization serving the members of state legislatures and their constituentsGo to sourceYou may need to fill out additional forms if you were previously denied EITC.

3Sell items around your home that you don’t use anymore. Look for items you own that you don’t use very often and try to sell them. You can try hosting a garage sale, posting them to online marketplaces, or taking them to resale stores. While they may not want to, encourage your children to find items they have that they don’t use anymore so they can sell them as well. As you sell your items, put the money toward your savings and any immediate expenses you need to pay.XOnly sell as much as you’re comfortable doing. Don’t get rid of anything you need to use on a regular basis.Let your children keep the money from anything they decide to sell so they can learn how to save as well.

4Take a work-from-home job to earn extra income if you can. Check online job boards to see what kind of part-time jobs you can work remotely from home. You may take online surveys, write blog posts, or sell your own crafts to make additional money on the side. Take any money you earn to pay off any debts before putting it in savings.XMany remote jobs require a stable Internet connection and a computer.Make sure you still have enough time to spend with your family and that you aren’t too exhausted after working multiple jobs.